FACING A PENNSYLVANIA SALES TAX AUDIT: WHAT TO KNOW

FACING A PENNSYLVANIA SALES TAX AUDIT: WHAT TO KNOW.

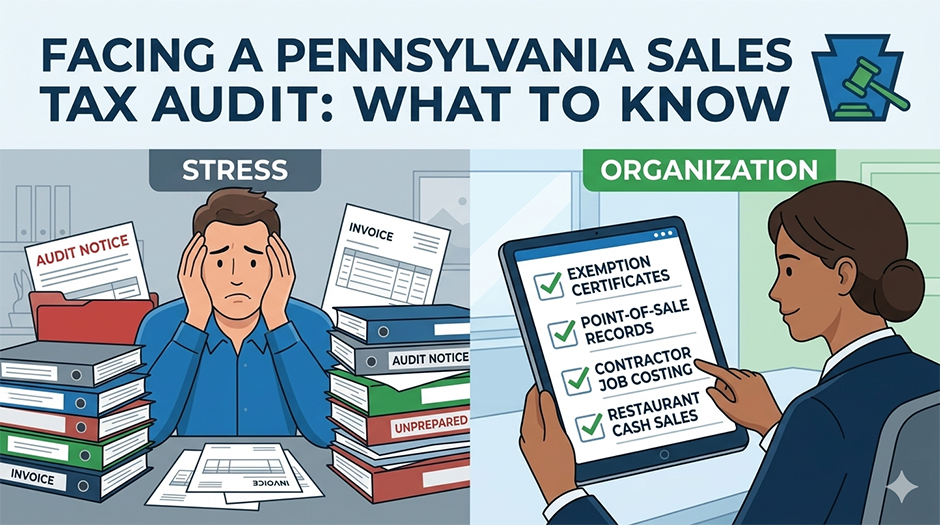

As a small business, you have plenty of challenges, some of which come at you faster than you can deal with. While sales tax audits are a routine part of tax enforcement, their impact on business operations is often more disruptive, costly, and time-consuming than many business owners anticipate.

At its core, a sales tax audit is the state’s way of verifying that a business has properly collected, reported, and remitted sales tax. In Pennsylvania, this responsibility falls on the seller, not the customer. That means if a business fails to collect the correct amount of tax—or fails to document exemptions properly—it can be held liable for the difference, along with penalties and interest. On top of that, the company’s principals may also be held liable for the company’s failure to remit sales taxes—all the more reason to involve an attorney experienced in sales tax audits.

Unlike large corporations with in-house accounting teams, many small businesses rely on a single bookkeeper, an outside accountant, or even the owner to manage financial records. When an audit notice arrives, it often requires pulling together years of documentation: sales records, invoices, exemption certificates, bank statements, and point-of-sale reports. This can quickly become a time-consuming and stressful exercise that pulls attention away from daily operations.

Although all types of businesses face the possibility of an audit, some are particularly susceptible. Restaurants, for example, are vulnerable during sales tax audits due to the complexity of their transactions. In Pennsylvania, most prepared food is subject to sales tax, but there are exceptions—such as certain grocery-type items or separately stated charges. Additionally, restaurants must correctly handle tax on takeout versus dine-in sales, as well as third-party delivery platforms. If records are incomplete or inconsistent, auditors may estimate sales using industry ratios or markup methods, which can result in inflated tax assessments.

Cash transactions also present a risk. Many restaurants still handle a significant amount of cash, and if those sales are not meticulously recorded, auditors may assume underreporting. Even minor discrepancies between reported sales and bank deposits can raise red flags. In some cases, auditors will compare a restaurant’s reported revenue to industry averages, and if the numbers seem low, they may expand the scope of the audit.

Contractors face a different but equally complex set of challenges. In Pennsylvania, the taxability of construction work generally depends on whether the contractor is improving real property or selling tangible personal property. Generally, contractors are considered the end users of materials they incorporate into real estate and must pay sales tax on those materials at the time of purchase. However, certain projects—especially those involving exempt entities or specific types of work—can change how tax is applied.

This distinction creates confusion, and errors are common. For example, if a contractor incorrectly treats a taxable sale as exempt or fails to pay use tax on materials, the state may assess tax on the total contract value or on estimated material costs. Without proper documentation, such as exemption certificates or detailed job costing records, it becomes difficult to challenge these assessments.

Assessments typically go back three (3) years and often include interest and penalties that substantially increase the total liability. In some instances, however, the lookback period may extend to six (6) years. If the auditor believes that a business significantly underreported sales, committed fraud or intentional evasion, or failed to keep sufficient records, they may extend the audit period to 6 years, dramatically increasing a company’s exposure.

Beyond the direct financial cost, audits can disrupt operations. Owners and staff may spend hours responding to auditor requests, gathering documents, and answering questions. This diversion of time and resources can affect customer service, project timelines, and overall productivity. For restaurants, this might mean less focus on food quality and guest experience; for contractors, it could delay project completion or bidding on new work.

For all these reasons, it is important to maintain accurate and organized records. Records can be your best defense in a sales tax audit. It is also important to get help. Contact a tax controversy lawyer if you receive a notice of a sales tax audit. Although many accountants are adept at handling such audits, most prefer to focus on tax preparation and steer clear of audits. Retaining an attorney also provides the added benefit of strict confidentiality in the form of the attorney-client privilege. Conversely, communications with a CPA or accountant are not fully privileged. An attorney will also look beyond the numbers and assess the state of the law in defending your position, challenging an auditor’s legal interpretations, and handling appeals and litigation, where necessary.

For more information on our Tax Law Services, visit here.